Marketing & Content

Since day one, the RazorPlan team has been dedicated to building technology that empowers advisors to spend less time building plans and more time building trust, ultimately delivering greater value to the clients they serve.

In part two of our six-part Planning as a Concept series, this post is focused on Investment Management. Download the ebook: Planning as a Concept.

Focusing on asset allocation, rate of return, and management fees, Investment Management concepts use investment value as the key metric. Clients that have a personal desire to increase wealth through investing, will be motivated to act due to the positive impact your advice will have on their investment accounts. Investment Management concepts include RRSP vs. Non-Registered/TFSA, Asset Allocation Rebalancing, and Cost of Investment Fees.

Investment Management plays an important part of any comprehensive financial planning engagement. The amount a client is willing to invest for their future will directly impact their ability to achieve goals related to major purchases, children’s education and retirement. Included with the Investment Management concept is a ledger that displays the change in financial position for investment savings, withdrawals and total assets, which will help your clients focus on the positive results they can expect from your recommendations.

This concept clearly communicates your Value of Advice by comparing the projected investment value of two scenarios using a line graph along with icons representing 5, 10 and 15 years of advice.

- Scenario 1 is the client’s current plan

- Scenario 2 is your recommendations

To illustrate the advantage of using the Investment Management concept over a product sales concept, we will examine a popular investment topic today, “Robo-advisors and the high cost of investment management fees.”

COST OF INVESTMENT FEES: CLIENT PROFILE

One of your clients recently referred you to his accountant Ruth. Ruth and Mark Stephens, age 43 & 44, have been married for 8 years and together they have $270,000 in RRSPs (saving $1,650 / month) and $25,000 in TFSA (saving $350 / month). Ruth manages and owns most of the couple’s investment assets which are invested with her local bank.

Recently Ruth was researching robo-advisor platforms after reading an article on the long-term impact that high investment fees could have on her retirement savings. Using an on-line fee calculator, she estimated that the fees she is paying on her portfolio will cost her almost $200,000 in lost investment growth by the time she retires.

Your client told her about the comprehensive financial plan you prepared for him that included a recommendation to consolidate investments using a low-cost ETF portfolio that you manage.

Using investment value is the best metric due to the focus on asset allocation, rate of return, and management fees.

Product Advice

Ruth contacted you to arrange a meeting at your office to discuss how your services compare to the various online roboadvisors and the fees you would charge on her portfolio. At the meeting you explained that your fees would be about 1% lower than the current fees on her portfolio and if she consolidated her investments with you the reduction in fees would have significant impact on the projected value of her investments over the long-term.

To illustrate this using RazorPlan, you create a planning file with 2 Scenarios; Scenario 1 would project a plan assuming a portfolio earning 5.5% rate of return until retirement and a 4% rate of return in retirement, Scenario 2 would assume a 1% increase in returns to represent your lower investment fees.

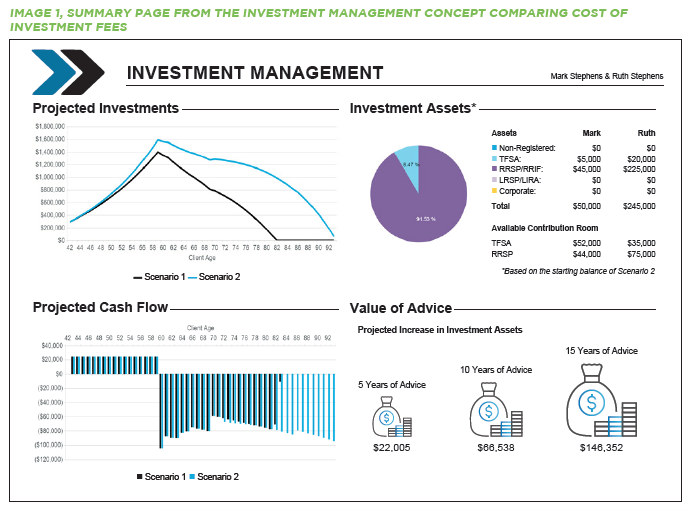

Using the summary page of the Investment Management concept (image 1), you can see that reducing investment fees by 1% annually is projected to increase their savings by $22,000 over 5 years. After 15 years, 3 years into retirement, the increase in investment savings is over $146,000, $54,000 less than the on-line calculator projected.

In addition to the change in total savings, the cash flow chart shows that their savings will now be sufficient to meet their needs for retirement income. With the higher fees demonstrated in Scenario 1, they are projected to consume all savings when Mark is age 82, 10 years short of Ruth’s life expectancy.

Planning Advice

By recommending a low-cost ETF portfolio, the projected long-term value of Ruth’s investments will be larger, but your value is limited to a product sale. Providing additional recommendations related to investment planning and the goals of the client will create Value over Product™ and help your clients better appreciate the financial advice, guidance and products you recommend.

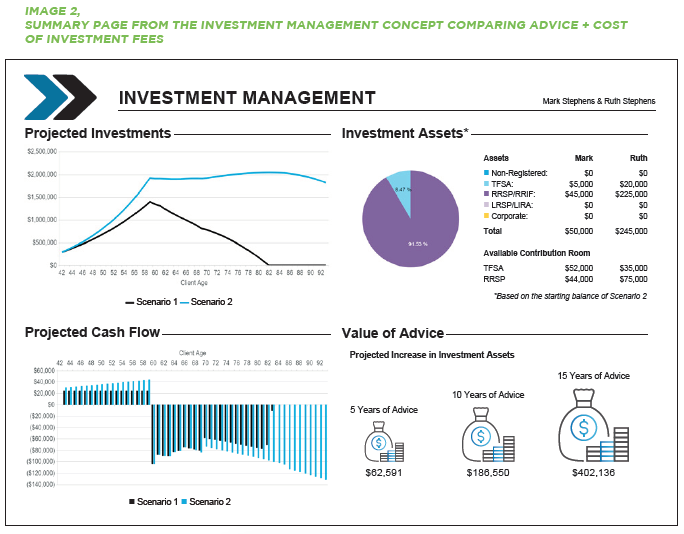

What if in addition to lower investment fees, you add the following recommendations in Scenario 2?

As Ruth’s income increases in the future, contributions to her RRSP & TFSA should also increase at the same rate.

Based on their current marginal tax rate, Ruth and Mark should redirect their TFSA contributions to their RRSP and then contribute 50% of their annual tax refund to their TFSA.

When they retire, they should time the conversion from RRSP to RRIF to minimize the 30% withholding tax on income drawn from retirement savings, and contribute any excess after-tax RRIF withdrawals to TFSA.

Adding these additional recommendations to the RazorPlan Investment Management concept improves the results by an additional $40,000 over 5 years and $250,000 over 15 years. Also, at life expectancy when investment assets are projected to run out with product advice, there is $1.8 million of Value over Product™ remaining, far exceeding the results provided by the robo-advisor.

INVESTMENT MANAGEMENT CONCEPTS INCLUDE:

1. RRSP vs. Non-Registered

2. RRSP vs. TFSA

3. Asset Allocation Rebalancing

4. Cost of Investment Fees

In part 3 of our series, we will be discussing Risk Management.

Planning as a Concept™ is a feature of RazorPlan financial planning software and uses Value of Advice to validate your recommendations and instill confidence in you as a financial professional.

Download the ebook: Planning as a Concept

Recent Posts

Improve Client Investment Planning with RazorPlan’s New Individual Assets Feature

Why business owners’ biggest planning gap comes after the sale

Protecting your Legacy: Planning for Private Company Shares

Optimizing your Retirement Strategy with RazorPlan Decumulation

Categories